#12-07 | PET ROCKS FOR SALE, QT RISK ON/RISK OFF, S&P500 MARGIN CALLS $SPX $ES_F $SPY $NQ $YM $VIX $DXY

Hi Mr. Investment Banker I Have A Pet Rock For Sale!

Goldman Sachs

Goldman Sachs CEO David Solomon commented on the current macroeconomic outlook, stating that he is cautious about the future. Goldman Sachs clients are taking steps to reduce their risk exposure. This suggests that there is some uncertainty in the market, and that investors are cautious about potential risks and volatility.

The fact that even the bank's clients are taking steps to reduce risk suggests that there is some concern among market participants about the potential for economic challenges in the near future.

Cautious About Macro Outlook, Says Clients Are Taking Risk Down.

Goldman Sachs CEO David Solomon

David Kostin from Goldman Sachs recently gave his outlook for 2023, stating that he expects the S&P500 to increase by 1% to reach a level of 4000 by the end of 2023. Kostin believes that while 2022 was marked by a decline in valuations, 2023 will be characterized by a lack of earnings per share (EPS) growth.

According to Kostin, the EPS for 2023 is expected to be $225, which represents 0% growth compared to 2022. The valuation of the S&P500 is expected to remain unchanged with a price-to-earnings (P/E) multiple of 17x.

However, in the event of a recession, Kostin believes that EPS could fall by 11% and the S&P500 could drop to 3150 (-21%). This suggests that the outlook for 2023 is relatively cautious, with a potential for economic headwinds to impact the performance of the stock market. It will be important for investors to monitor economic indicators closely in order to assess the potential risks and opportunities for their portfolios in the coming year.

It is interesting to note that on August 22, I tweeted about potential lower targets for the S&P500 index, which included levels of 3500, 3200, and 3160. The target is only $1 away from the 2023 outlook provided by Goldman Sachs, which predicts a potential drop to 3150 in the event of a recession.

Investing in the market and understanding potential risks involves conducting research, which is a key component. As a result, it highlights the possibility of a significant decline in the stock market if an economic downturn occurs. Monitoring economic indicators and developments is essential for making informed investment decisions.

JPMorgan

This morning, JPMorgan CEO Jamie Dimon gave an interview on CNBC in which he discussed the state of consumer spending.

JPMorgan CEO Jamie Dimon Says Consumers Are Spending Down Their Excess Savings From Pandemic Stimulus Programs, And That Will Run Out In 2023.

This comment is in line with recent data on #11-28 consumer spending, which has shown that while consumers are spending money, they are mostly buying essential items rather than discretionary items and in return receiving less quantity.

Jamie Dimon comments indicate that the current state of consumer spending is likely to be short-lived, and that it may be difficult to sustain in the long term. This could have implications for the broader economy, as consumer spending is a key driver of economic growth.

Crypto Is A Complete Sideshow, Tokens Are Like Pet Rocks!

JPMorgan CEO Jamie Dimon

JPMorgan's Co-CEO of the Consumer Division recently commented on trading revenue, stating that it is up around 10% in Q4 compared to the same period last year.

This increase in trading activity is interesting, as it may be an early indication of investors engaging in tax loss harvesting. Tax loss harvesting is a strategy in which investors sell assets that have declined in value in order to realize losses that can be used to offset capital gains and reduce tax liability.

The fact that trading activity is up at a time when the markets are selling off at resistance levels is consistent with the idea that investors are using tax loss harvesting to mitigate the impact of market volatility. This increase in trading activity could also be seen as a sign of increased caution among investors, who may be looking to take profits and reduce risk in their portfolios.

The USA Redbook (YoY) was released, showing 5.7% growth compared to the prior reading of 10.4%. This decline in the growth rate could indicate that retail activity has slowed, which could in turn suggest that the overall economy is slowing down. This would be consistent with the cautious outlook expressed by JPMorgan's CEO earlier in the day. Overall, these developments suggest that investors and businesses should remain vigilant and monitor economic indicators closely in order to assess potential risks and opportunities.

China Zero-COVID

As China moves to ease quarantine, the US is being hit with headlines of increase in COVID infections. Although China is easing policy they are not backing down, the markets would like to see China abandoning Zero-COVID.

According to New York Times tracker, U.S. COVID-19 cases were 53,019 per day on Monday, about 28% more than two weeks ago, as headlines hit the wire pre market. COVID infection currently hospitalizes approximately 35,000 people in the U.S., and 261 people died on Monday.

China is reportedly considering a gross domestic product (GDP) target of around 5% for the coming year, as the government shifts its focus towards economic growth. This target is lower than previous years, but it reflects the challenges and uncertainties facing the Chinese economy.

China's economy has been hit hard by the ongoing global pandemic, and the country is facing slower growth and increased risks. As a result, the government is shifting its focus from maintaining high levels of growth to ensuring that the economy remains stable and sustainable.

A GDP target of around 5% would indicate that China is prioritizing stability and sustainability over rapid growth. It would also signal that the government is taking a more cautious approach to policy making, and is prepared to make trade-offs in order to support the broader economy.

Risk On / Risk Off

The recent shift from a "risk on" to a "risk off" environment in the financial markets occurred over the course of just four trading days. This rapid change in investor sentiment is an example of the high level of dynamic thinking that is essential for understanding the current risk environment.

Risk on and risk off refer to the level of risk among investors. When investors are willing to take on more risk in pursuit of higher returns, this is known as a risk on environment. In contrast, when investors are more cautious and are less willing to take on risk, this is known as a risk off environment.

Due to concern about the economy, financial markets, or geopolitical climate, investors are more risk averse and seek safe assets, such as government bonds. Risk-off may indicate an imminent recession, as it can indicate significant economic or financial stress.

Eurodollar & DXY

The Eurodollar, which is a deposit of US dollar-denominated funds held in banks outside of the United States, is another important factor to consider. Eurodollars are a key source of financing for international trade and can have a significant impact on the S&P500 and other financial markets.

When the supply of Eurodollars is tight, it can drive up interest rates. On the other hand, a plentiful supply of Eurodollars can drive down interest rates. Changes in the supply of Eurodollars can impact interest rates and exchange rates, which can then affect investor sentiment and the overall risk environment.

During times of high demand for the US dollar, there may be a shortage of dollars available, which can have a significant impact on market risk. This is because the dollar is the dominant reserve currency and is widely used in international financial transactions.

A shortage of US dollars can affect the cost of borrowing, exchange rates, and the availability and affordability of imported products. A strong dollar can also impact various factors, such as export costs and consumer availability.

When the supply of US dollars is limited, interest rates may increase, making borrowing more expensive. This can lead to a decrease in profitability and stock prices, creating a negative risk environment for companies.

Small Cap - Mid Cap (Businesses Under $10 Billion Market Cap)

In the event of a mild recession and the value of the US dollar is high in the context of a bear market for the S&P500, it could have a detrimental effect on companies with a market capitalization less than $10 billion.

In consequence, a mild recession can adversely affect companies' revenues and profits. A mild recession typically involves a slowdown in economic activity and a decline in gross domestic product growth.

In addition to making exporting products and services more difficult, a strong US dollar can have an adverse effect on global supply chains. When the dollar value is high, buying foreign goods costs more in local currency, reducing profits for the company.

As a result of a strong dollar, companies may have to adjust their business strategies and operations to mitigate the adverse effects it may experience. A reduction in sales and revenue could also result from implementing cost-cutting measures, diversifying the company's supply chain, or hedging against currency risks.

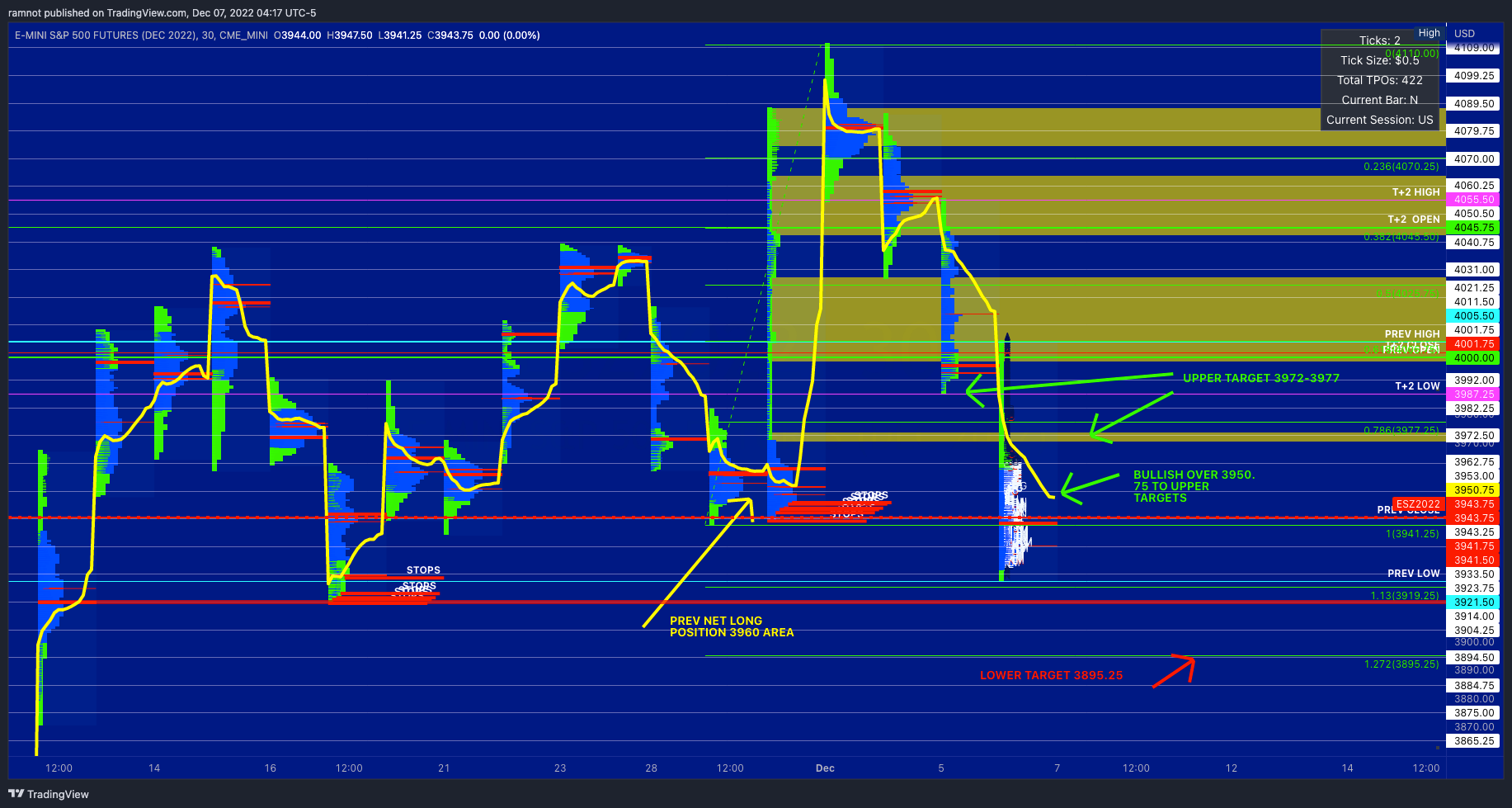

S&P500 E-Mini Futures

Yesterday's key theme was that if the market failed to recover above the T+2 Low, the price action could become messy and potentially lead to further declines. This is exactly what happened, as the market opened lower and continued to sell off throughout the day. The lower target, if the market failed to recover above the T+2 Low, was the 4th short position in the 3972.50 zone.

The market did indeed flush through this level and began to build inventory in the same area where net longs were positioned before Powell's speech. This suggests that the market is becoming increasingly bearish and that investors are losing confidence.

The failure to recover above the T+2 Low is a negative sign, and it indicates that the market may be at risk of further declines. It will be important for the market to recover above this level in order to avoid a more severe sell-off.

Based on the chart above, it is evident that inventory has been drastically short since yesterday. We took out every major stop to the downside and started to build a position around 3942. If wholesalers can hold 3942, we can rotate back up to test RTH VWAP at 3950.75, which opens a door to 3972-3977. If the previous day’s low is broken, our lower target of 3895.25 will be in play.

Nice analysis thanks for the contribution 🙏🏽